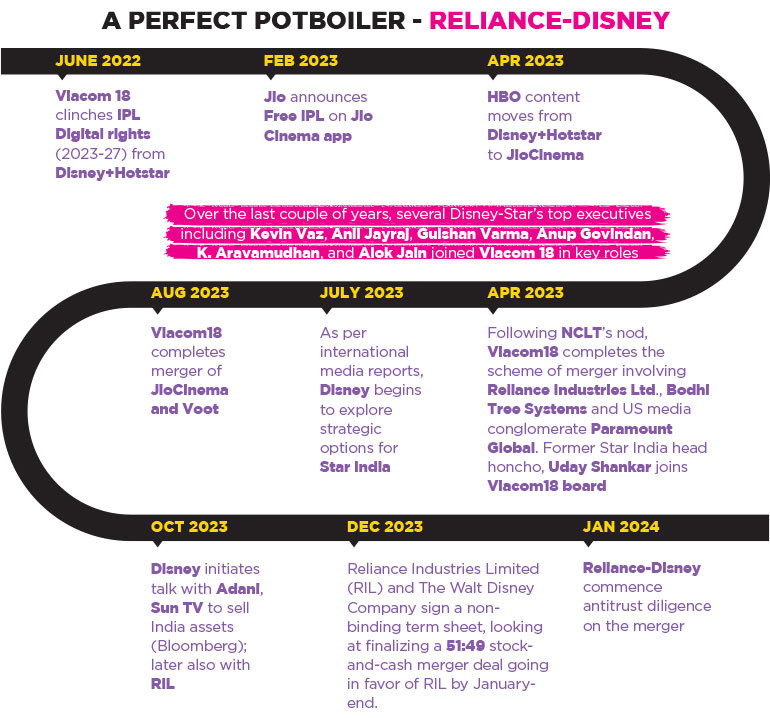

After months of speculation, Reliance Industries Limited (RIL) and The Walt Disney Company, reportedly, signed a non-binding term sheet in the last week of December with the intent to finalize the high-profile merger between Disney Star and Viacom18 by January-end. The deal is said to be a 51:49 stock-and-cash merger going in favour of RIL. As per industry experts, if the merger goes through, the Reliance-owned entity will emerge as the largest in the Indian broadcasting market, with a combined topline of approximately Rs. 25000 cr. and a 43% share of the TV ads market.

Currently, Disney Star owns over 70 TV channels in eight languages, the Disney+ Hotstar OTT platform, and a film studio. Reliance’s broadcast division Viacom18 owns 38 TV channels in eight languages, a Digital streaming platform - Jio Cinema - and a film studio, Viacom18 Studios. While Disney Star has a 32% share in the ad market, Viacom18 has an 11% ad market share. The merged entity will have a combined 43% ad market share with over 100 TV channels, two streaming platforms and two film studios. Disney Star’s operating revenue for FY23 was Rs 19,857 crore while that of Viacom18 was Rs 4,554 crore.

ROAD AHEAD

Reliance Industries Ltd. and The Walt Disney Co. rang in the new year by starting antitrust diligence on the merger. As per antitrust experts who spoke to Reuters, a key area of antitrust scrutiny for the merger would be their streaming businesses and their power over advertising during cricket. CEO Bob Iger had, a month before the signing of the term sheet, stated that while Disney’s TV channels were doing well in India, other parts of the business were struggling and it was seeking to ‘improve the bottom line.’ Star India became a part of Disney after the latter acquired 21st Century Fox for $71.3 Bn in 2019. As per the company’s latest filing, its net profit for FY23 fell by 31% to Rs 1,272 cr., even as its income saw a 9% increase to Rs 20,699 cr.

Given the protracted Sony-Zee merger that the industry is witnessing, which experts say is unlikely to go through, the latest developments suggesting that Reliance and Disney India could become one entity by February 2024 do seem like an overstatement. A non-binding agreement, as the name also suggests, is an agreement in which the parties are not legally obligated to perform, and primarily sets out the understanding or the principal intentions of the parties. It is beneficial in situations where the aim is to outline specific terms for a particular arrangement, yet uncertainties linger. Speaking to e4m, Nikhil Varma, Managing Partner, MVAC Advocates & Consultants, said, “On an average, the process can take several months to over a year or more to receive all necessary approvals and finalize the merger. It’s not uncommon for large media mergers to face regulatory challenges and negotiations that contribute to the overall time frame. Therefore, providing a precise time frame without specific details about the merger in question is challenging.”

Speaking to e4m, Nikhil Varma, Managing Partner, MVAC Advocates & Consultants, said, “On an average, the process can take several months to over a year or more to receive all necessary approvals and finalize the merger. It’s not uncommon for large media mergers to face regulatory challenges and negotiations that contribute to the overall time frame. Therefore, providing a precise time frame without specific details about the merger in question is challenging.”

MEDIA POWERHOUSE IN THE MAKING

Ever since news about Disney’s Burbank headquarters exploring strategic options for its India assets broke in July last year, Disney Star has reportedly been in talks with Adani and Kalanithi Maran’s Sun TV. The proposed merger with RIL, however, is the coming together of two parallel tracks.

Former Disney (Asia Pacific) and Disney Star head honcho, Uday Shankar who joined the Viacom 18 board in April 2023 has always been vocal about the streaming-first future of entertainment in India. Bodhi Tree Systems, the Qatar Investment Authority (QIA)-backed investment platform jointly run by him and media mogul James Murdoch, was launched in February of 2022 with the stated goal of investing in media and consumer technology opportunities in Southeast Asia, with a particular focus on India. It owns 13.08% stake on a diluted basis in Viacom18 today.

Shankar’s appointment was concurrent with the integration of Jio Cinema into Viacom18 in April 2023, when following NCLT nod, the scheme of merger involving Viacom 18 (TV18 and US media conglomerate Paramount Global), RIL group entities, and Bodhi Tree Systems was also completed. Post the merger, Viacom18 got access to Rs 15,145 cr. cash for its planned growth, comprising Rs 10,839 cr. contributed by RIL group entities and Rs 4,306 cr. contributed by Bodhi Tree Systems. A few months later in August, Viacom 18’s existing streaming service, Voot, was also merged with Jio Cinema.

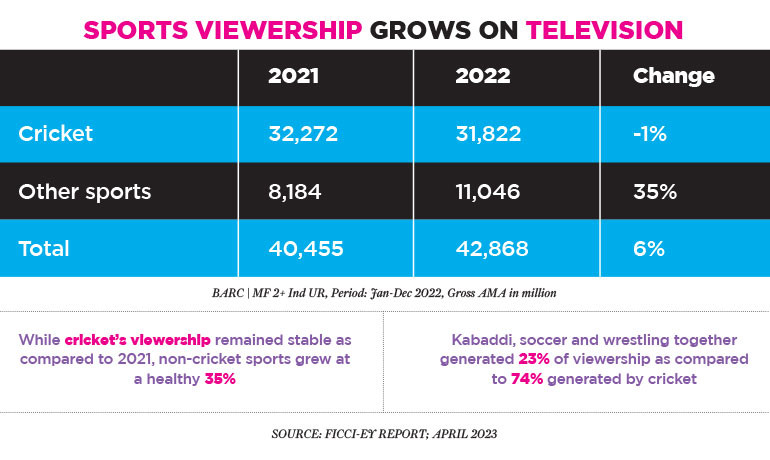

Backed by Reliance’s might and the strategic and operational guidance provided by Shankar and Murdoch, Viacom 18 made great strides, further shaking up the sector that was already under disruption. Foremost among them was streaming the most expensive media property, IPL, for free. Ever since winning the IPL Digital rights, hitherto with Disney+Hotstar, in 2022, Viacom 18 has been investing disproportionately in acquiring tentpole cricketing properties. The network also owns the media rights for the Women’s Premier League (WPL), BCCI Bilateral cricket, and Cricket South Africa. Last year, the total media rights valuation for all major cricketing properties (men’s and women’s) reached a staggering Rs. 80,000 cr., which is comparable to the total Indian AdEx for 2022 at Rs. 89803 cr. (Pitch Madison Advertising Report 2023).

Apart from IPL, Jio Cinema also became the new home for HBO and Warner Bros. content in India after Disney decided against renewing the deal last year. Over the last couple of years, several Disney-Star’s top executives including Kevin Vaz, Anil Jayraj, Gulshan Varma, Anup Govindan, K. Aravamudhan, and Alok Jain joined Viacom 18 in key roles. The constant content and talent drain finally culminated in RIL and The Walt Disney Company signing a non-binding term sheet late last December. As per media reports, the proposed plan involves creating a step-down subsidiary of RIL’s Viacom18, which will absorb Star India through a stock swap. In this arrangement, Reliance aims to be the majority shareholder with at least 51%, leaving Disney with the remaining 49%. RIL is likely to acquire the controlling stake through a cash payment. Speculations are rife that both entities will together invest around $ 1.5 billion into the deal, under which Ambani’s firm will gain distribution control of Star India’s channels. Once the term sheet is agreed upon, confirmatory due diligence will be conducted, and the valuation process will officially commence with input from independent valuers. While industry experts and the broadcaster itself may believe that they are investing in a long-term vision, writing for e4m, Anup Chandrasekharan, COO – Regional Content, IN10 Media Network, called it a ‘bloodbath.’ “The biggest mistake that happened in our industry is the ridiculous pricing at which cricket and movies were bought in 2023. In the name of customer acquisition, all of them dipped themselves into a bloodbath – proclaimed that blood is marketable and it’s a disaster for the entire industry as it just didn’t make any financial sense to buy those assets at that value. This short-sightedness will result in a disaster from which the industry will take time to recover.”

While industry experts and the broadcaster itself may believe that they are investing in a long-term vision, writing for e4m, Anup Chandrasekharan, COO – Regional Content, IN10 Media Network, called it a ‘bloodbath.’ “The biggest mistake that happened in our industry is the ridiculous pricing at which cricket and movies were bought in 2023. In the name of customer acquisition, all of them dipped themselves into a bloodbath – proclaimed that blood is marketable and it’s a disaster for the entire industry as it just didn’t make any financial sense to buy those assets at that value. This short-sightedness will result in a disaster from which the industry will take time to recover.”

On the merger itself, he added, “Disney India on the block surprises all of us. Their broadcast segment is profitable, and it defies all logic to see them do a desperate deal with Jio. Having bought the network from Fox at a steep valuation, giving it up so easily and so quickly makes me question the team at Burbank. The big question is how Disney then bought this dream earlier of buying Star India at such valuations. The greatest flaw observed in Disney India is also not investing in content aggressively to populate the momentum around cricket and thus failing to hit the bull’s eye. Disney India started playing the P&L game and it’s obvious that their long-term vision got blurred.”

MERGING EFFICIENCIES IN A CHANGING MILIEU

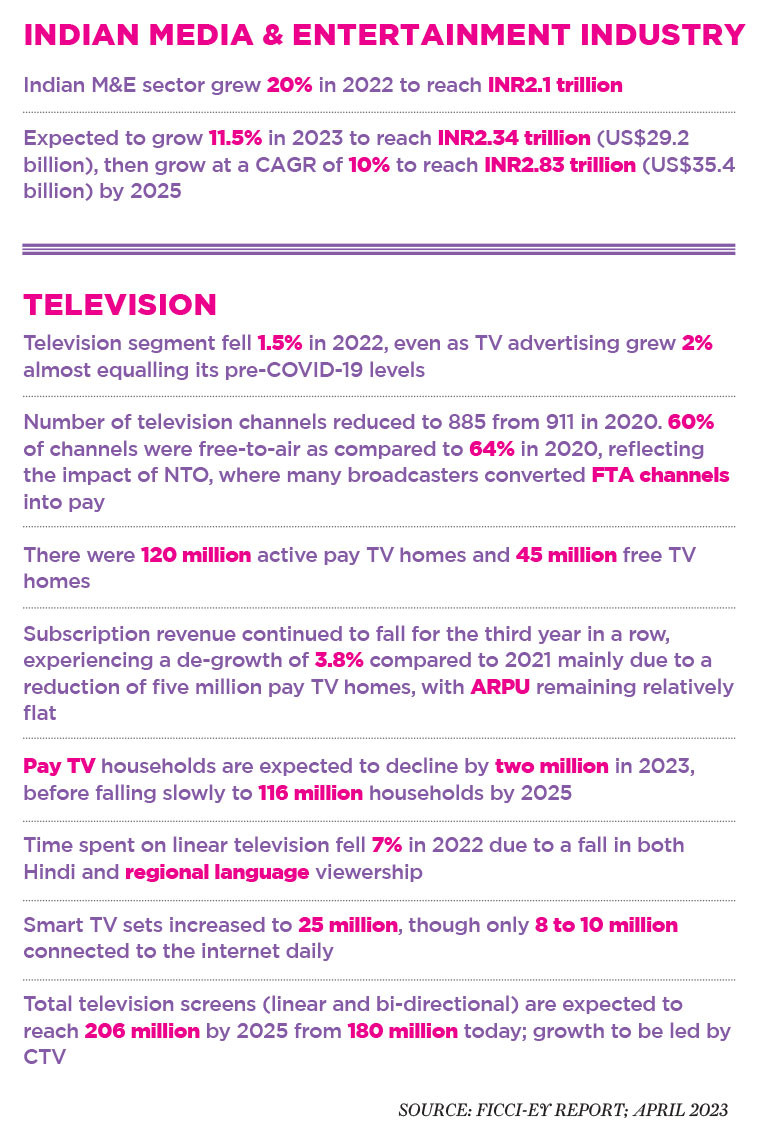

The broadband and tech revolution has put the linear pay TV segment under immense pressure as it battles bi-directional and free television on both ends of the spectrum. This is not to say that demand for content is getting any less. According to the FICCI-EY April 2023 report, the Indian M&E sector grew 20%, reaching INR 2.1 trillion in 2022; 10% more than its pre-pandemic levels in 2019. It is expected to grow 11.5% in 2023 to reach INR 2.34 trillion and further grow at a CAGR of 10.5% to reach INR 2.83 trillion by 2025. Advertising exceeded the INR1 trillion benchmark in 2022 for the first time, although at 0.4% of India’s GDP, the growth is much lesser than the developed markets, and hence there’s ample scope for growth. Indians now consume nearly 20GB of data per month on average, the highest in the world already, and expected to reach 46 GB by 2027.

While the opportunities are aplenty, television - linear pay TV precisely - is beset with challenges. The overall television segment fell 1.5% in 2022. Subscription revenue continued to fall for the third year in a row, experiencing a de-growth of 3.8% compared to 2021 mainly due to a reduction of five million pay TV homes, with ARPU remaining relatively flat. Pay TV households are expected to further decline by two million in 2023, before falling slowly to 116 million households by 2025. Time spent on linear television fell 7% in 2022 due to a fall in both Hindi and regional language viewership.

On the contrary, smart TV sets increased to 25 million. There were 120 million active pay TV homes and 45 million free TV homes. Total television screens (linear and bi-directional) are expected to reach 206 million by 2025 from 180 million today. This growth would, however, be driven by connected TVs which could cross 40 million by 2025 and free television which could cross 50 million.

Sharing his thoughts at the turn of the year, Sandeep Gupta – COO, Broadcasting Business, Shemaroo Entertainment Limited, predicted a ‘FAST and Free Dish-led growth’ for the coming years. “Even though at a very early stage, FAST channels could well pick up consumption in 2024, with multiple platforms already offering such services or planning to offer shortly. Going forward, Freedish is likely to surpass a base of over 50 million households by 2025,” he said.

Sharing his thoughts at the turn of the year, Sandeep Gupta – COO, Broadcasting Business, Shemaroo Entertainment Limited, predicted a ‘FAST and Free Dish-led growth’ for the coming years. “Even though at a very early stage, FAST channels could well pick up consumption in 2024, with multiple platforms already offering such services or planning to offer shortly. Going forward, Freedish is likely to surpass a base of over 50 million households by 2025,” he said. Given the scenario, the impending developments are to be seen in a positive light. “It will solve the problem of lower growth rates on the linear TV side, which has come down to 3%-4%, as both these players will potentially gain more market share with smaller players moving purely to digital or partnering with larger ones in the ecosystem. It will also work favourably for the OTT ecosystem, as most OTT platforms (global giants and broadcaster-led) are making hefty losses due to high content costs. Further, Jio Cinema’s free content offering has also disrupted India’s OTT market, as players are struggling to scale up SVOD revenues,” says Karan Taurani, Senior Vice President, Elara Capital.

Given the scenario, the impending developments are to be seen in a positive light. “It will solve the problem of lower growth rates on the linear TV side, which has come down to 3%-4%, as both these players will potentially gain more market share with smaller players moving purely to digital or partnering with larger ones in the ecosystem. It will also work favourably for the OTT ecosystem, as most OTT platforms (global giants and broadcaster-led) are making hefty losses due to high content costs. Further, Jio Cinema’s free content offering has also disrupted India’s OTT market, as players are struggling to scale up SVOD revenues,” says Karan Taurani, Senior Vice President, Elara Capital.

Emerging on the Indian media and entertainment scene post the economic liberalisation of 1991, Star India has, through the decades, built a towering legacy for its television brands and later also for Disney+ Hotstar. The highly futuristic Ambani-Shankar-Murdoch trio joining them will mark the next big development in the history of Indian broadcasting that will usher in a phase of rapid technological advancements and globalized content in the industry. It remains to be seen how far will the other two legacies - Sony and Zee- be part of this revolution either independently or as one.

SONY-ZEE: A MISSED OPPORTUNITY?

Industry insiders are already predicting a grim outcome as regards the $10Bn mega-merger between Zee and Sony. Even as the ongoing discussions continue till January 20, Sony Group is reportedly keen to place its India CEO NP Singh as the Chief Executive Officer of the merged entity in the wake of SEBI barring ZEEL MD Punit Goenka from holding any key managerial positions. While the ban on Goenka has been lifted by the Securities Appellate Tribunal (SAT), Sony still views the ongoing SEBI probe as a corporate governance issue.

Sources say that apart from the standoff over CEO appointment, ZEEL’s poor financial performance and the $1.5 billion sub-licensing deal for ICC Cricket signed by the company in August 2022 with rival Star. have further miffed Sony Corp.

With Goenka wanting Sony to honor the original agreement as per which he was to serve as MD and CEO of Sony-Zee for a period of five years from the effective date, there’s a possibility of the deal falling flat after two years of negotiations and despite obtaining key regulatory approvals. According to Elara Capital, “In case Sony calls off the deal, shareholders may resort to a consortium to engage with Sony or another strategic partner post that. The deal is between two entities and Mr. Punit Goenka being the CEO of the merged co. is a part of the deal, but not a key reason or a trigger for the deal being called off. The likelihood of the deal going through remains much higher without him, as the promoter group has a stake of mere ~4% in the company, thus limiting bargaining power with shareholders, who own a large chunk of the company (77% owned by institutional holders).”

Taurani reckons that with the Reliance-Disney merger on the horizon, the collapse of the deal will hurt both the entities even more. “Converging growth rates on the linear TV side and hefty losses on Digital will impact both Zee and Sony negatively. They will not be able to grow faster than the market on the linear TV side and on the digital side, they will struggle to scale up. It’ll be a big win for Reliance, specifically on the digital side because after acquiring IPL rights, Jio Cinema is the market leader now at least in terms of ad revenue scale. They’ve got the highest ad revenue number and viewership number compared to any other OTT platform in the country today. They will be able to compete with and pressurize other platforms like Zee5, SonyLIV if the merger does not go through.”